By John Dewhirst

For the last twenty years at least the practice at Valley Parade has been for minimal disclosure of detail in the published financial statements of the operating company, Bradford City Football Club Limited (registered number at Companies House: 05102915).

The practice of filing abridged accounts is neither illegal nor unique but is an option for any private company with turnover of less than £10.2m per annum and a balance sheet of less than £5.1m, criteria that BCAFC fulfils with little difficulty.

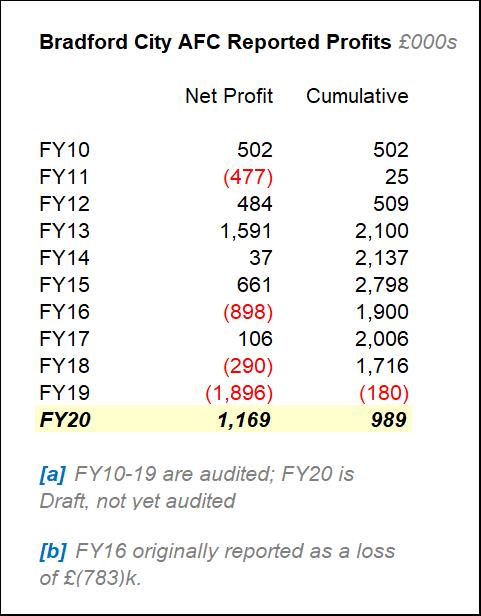

Its most recent published accounts for example are for the financial year ended 30th June, 2019 (‘FY19’) in which it had turnover (i.e. trading income) of just £6.7m and a negative balance sheet of £(1.1)m which is to say an excess of liabilities to assets and technically insolvent.

The instinctive reaction of many finance directors is to disclose as little as necessary about the financial affairs of a company and to reveal information on a need to know basis. Like most football clubs, the affairs of Bradford City are subject to an inordinate degree of scrutiny and speculation and hence there is good reason to be cautious about what commercial information is made public.

On the other hand, the minimal disclosure practice has served only to encourage conjecture and conspiracy theories about the club’s financial circumstances. Many of the comments made about the club’s affairs are groundless and quite often, simply ludicrous.

I have experience undertaking diligence and business reviews on behalf of banks and investors and I am familiar with the club’s accounts having undertaken an independent examination on behalf of Bradford City AFC and the PFA in 2003 and 2004.

Julian Rhodes was receptive to my suggestion at the end of last season to undertake an independent review of the accounts and to summarise them in a feature such as this. The club’s auditors, Bostocks Boyce Welch have provided me with full assistance and had it not been for the lockdown and staff working off-site this would have been published much sooner.

With concerns among supporters about the implications of Covid it is now particularly topical. The purpose is to provide some background about the club’s financial circumstances and hopefully dispel some of the more extreme claims and expectations that exist. Quite possibly it will serve as a reality check and maybe even provide some reassurance.

A small business

First and foremost, what surprises many people is that in terms of size, Bradford City is a relatively small business. The club’s annual turnover is less than what the highest paid players in the Premier League can expect to earn in a year.

Not only that, it is a small business with a record of marginal profitability and in a nutshell that is the most profound financial analysis that can be made. By any standard, it is not an organisation with the wherewithal to act as a large corporate entity and that has been the case for the vast majority of the club’s existence.

Even within Bradford, BCAFC is not a big business. The club’s significance to the local economy is primarily of an indirect nature, for example by drawing people into the city, generating publicity and on occasions, creating a feelgood factor.

Whilst Valley Parade generates rates for the local authority (£0.1m pa), Bradford City is not a major employer. The club’s social impact on the district is principally through community involvement.

Collectively all of this represents considerable leverage but does not alter the fact that as an organisation, the club is no bigger than many small owner managed businesses. Neither is it a ‘big club’.

The historical context

History is relevant to provide some context. For a start, the late development of soccer in Bradford denied the possibility that a local side might establish itself as a pioneer with the prestige that would have accrued.

In 1892 for instance, Bradford FC at Park Avenue was said to have been the wealthiest football club in Great Britain. Had it been an association – as opposed to a rugby – football club it is not inconceivable that Bradford FC would have been successful and become a leading side in England.

In 1903 Bradford City AFC was established with minimal financial backing. The lack of resources meant that the club struggled to simultaneously build a team and develop Valley Parade. In 1907 the abandonment of rugby at Park Avenue meant that City no longer had a monopoly in the district as the only professional association football club.

The existence of a second club – Bradford Park Avenue – handicapped the efforts of BCAFC to raise sufficient share capital in 1908 which had far reaching implications. Most of the funds raised were used to develop Valley Parade, all of which meant that insufficient resources were available to sustain the success of the side after winning the FA Cup in 1911.

World War One had a major negative impact on the club’s financial affairs and all told it meant that City lost its first division status instead of being able to consolidate. Relegation in 1922 from Division One precipitated a series of financial crises and Bradford City fell down the rankings of English football.

The story of the last one hundred years has been dictated by the fact that the club has been under-capitalised, or in layman’s terms impoverished. It has meant that the finances of Bradford City AFC have never been sufficiently resilient to absorb the cost of failure or to provide the resources to buy success.

Instead the club has been trapped in a negative cycle of trading losses that have forced player sales and an inability to invest, a consequence of which has been loss of public interest and continuing financial difficulties. That cycle has never really been broken and the club has historically relied upon the bonus of cup glory or player sales as well as supporter fund-raising to stay afloat.

Historically, the club has suffered the burden of a ground – built on a steep hillside – that has been costly to maintain and upgrade. Whilst the rebuilding of the stadium in 1986 had a massive benefit, allowing the club to increase commercial revenues as well as attendances, the irony is that since 2004 Valley Parade has become an even bigger burden in cost (both in absolute as well as relative terms) than ever before.

For much of the post-war period, Bradford City has been an unglamorous lower division side. The toxic record of Bradford football (and maybe perceptions of Bradford itself) has also deterred wealthy people from financing the club or getting involved. With the benefit of hindsight, had BCAFC secured promotion to Division One in 1988 it could have been a significant turning point and the club might then have been able to establish itself firmly in the top half of the Football League.

At that time, the gulf between the top two divisions was much less pronounced but the failure to advance came down to the shallow foundations, a lack of resources and the absence of a benefactor willing to bankroll success. The same themes became apparent once more at the turn of this century.

Geoffrey Richmond was responsible for betting the finances of the club in his six weeks of madness during the summer of 2000. However, for the club to have sustained itself as a Premier League side meant that a big financial gamble was unavoidable. Had Richmond’s signings been successful, Bradford City might similarly have been transformed.

However, the reality was that whilst Richmond sought to emulate other clubs in making his move, his was a gamble that he could not afford to lose. Plenty of big clubs make big gambles although typically don’t face the same ‘all or bust’ high risk stakes.

Once again it came down to BCAFC lacking financial resilience but the other salutary fact was that Richmond was reliant upon borrowed money to finance his adventures.

As I recall from my involvement at the time undertaking an independent review of the club’s finances, I can say without exaggeration that the financial circumstances of Bradford City were among the worst that I have ever seen. In the last twenty years I have been involved as an adviser with more than 300 situations of financial and operational restructuring and of all those, I can think of only a couple that had finances in a more desperate state in relative terms than BCAFC in 2002. In fact, both of those were cases of fraud.

The consequence of insolvency in 2002 and again in 2004 was that the club was saddled with a considerable rental burden which has been subject to upwards revision every five years.

The current rent for example is £434k per annum compared to £300k in 2003. (Additional to the rent the club is, pursuant to the lease, responsible for paying the costs of insuring the ground and all other outgoings and also under an obligation to the landlord to keep the stadium in good repair.) In the immediate aftermath of the insolvency there was also a commitment to repay liabilities under the terms of a Creditors’ Voluntary Arrangement (CVA).

Prior to the sale of BCAFC in 2016 the finances were once again dictated by the lack of capitalisation and the absence of a wealthy benefactor. Indeed, Messrs Lawn and Rhodes sold the club because they lacked the personal financial resources to invest on a long-term basis. An interest-bearing loan of £1.0m from Mark Lawn in 2008 was used to finance a promotion challenge and this was repaid in 2013 with the benefit of the League Cup revenues.

The balance sheet has remained a handicap. Prior to 2016 the directors failed to attract a buyer, primarily on account of the fact that the club did not have assets (and that considerable funding was necessary to make good a lack of investment in prior years).

Likewise, the weakness of the balance sheet was such that BCAFC would have been unable to secure third party borrowings without the directors providing personal guarantees. Besides, after the implosion of the club at the beginning of the century the chances of a lender advancing funds on affordable terms was remote (and will continue to be so).

The implication of limited resources

For any business operating in an uncertain and volatile environment where success is often a matter of good fortune, the lack of a capital buffer is a massive handicap. It means that there is no room for error and in practice it not only leaves a company vulnerable to cash crises (i.e. inability to pay wages, the rent or other creditors when commitments fall due) but conspires against long-term planning.

If a business has high monthly fixed costs (i.e. payroll and rental commitments) it can make things very difficult and at worst can lead to existence on a week-by-week basis.

It is not necessarily an easy task to manage the financial affairs of a football club. The variables and uncertainties can make forecasting difficult to say the least, with no guarantees that there will be sufficient cash to pay the bills.

In that regard, in the last couple of years the financial support of Stefan Rupp has provided a degree of security such that in the final event, the wages can be paid. The McBurnie windfalls have also been fortuitous and whilst the timing owes much to good fortune, they underline the strategic benefit of the club’s transfer dealings.

Image by Thomas Gadd (copyright Bradford City)

The difference between now and prior eras has been the sheer scale of amounts involved, whether the level of wages, the player transfer fees or the extent of operating losses. Previously the club would rely upon bank overdraft funding secured by director guarantees, but this is no longer an option.

In 2008 Mark Lawn provided a loan to finance a promotion challenge and during FY19, Stefan Rupp provided a loan of £1.76m to cover the losses made in that year. (An additional bridging loan of £0.20m was received in June, 2020 pending receipt of McBurnie monies and then repaid in July, 2020.)

What do the accounts tell us?

In the period since the insolvency in 2004 and prior to the sale of the club in 2016, the club was broadly profit neutral. The most apt way of describing the financial performance of Bradford City in the period 2004-16 is that it operated within its means and with a willingness to invest a prior year surplus.

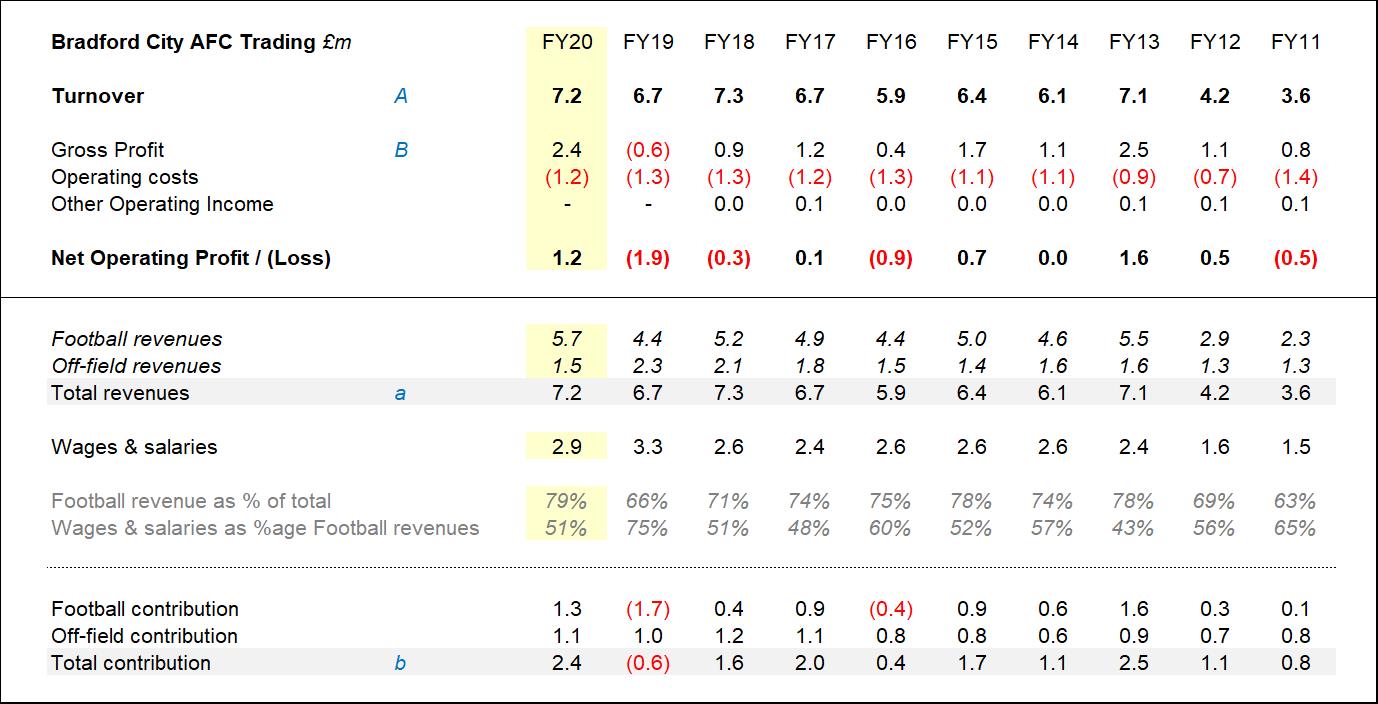

The financial record was solid and consistent although insufficient to finance overdue investment in Valley Parade – let alone a radical transformation of the club – without new monies being introduced. In the ten years to FY20 the turnover of the club was nearly doubled, albeit from a low base.

Internally the club prepares very detailed management accounts to monitor its costs. My understanding is that Edin Rahic instituted certain changes to the reporting of information (as well as a restatement of the prior year, FY16 accounts) that has necessitated some adjustment in this exercise to ensure like for like comparison.

Essentially the trading income is categorised as ‘football’ on the one hand and ‘commercial’ (i.e. off-field) on the other. The former includes gate receipts, season ticket sales and player transfer fees. Total football revenues in the period FY12-20 inclusive amounted to £44.9m of which £9m (20%) was generated by player sales. Commercial revenue comprises sponsorships and off-field income generating activity.

The accounts for last season (‘FY20’) have yet to be audited but the draft accounts disclose a net profit in the year of £1.2m, driven principally by receipt of monies in relation to Ollie McBurnie. Prior to FY20, in the four preceding financial years the club has disclosed losses of £3.0m, of which £1.9m in FY19 alone. A factor in the higher losses in FY19 was the much higher wage bill that increased by 25% from £2.6m in FY18 to £3.3m in FY19, coupled with the deterioration in receipts that accompanied a relegation season.

Player wages have been a growing proportion of football revenues and in FY19 represented 75%. In FY20 this percentage fell arising from the income attributable to Ollie McBurnie included within football revenue. The burden of the rental commitment has remained significant and in FY19 was equivalent to just under 10% of football revenues.

![]()

The cup run and promotion in 2013 boosted turnover to £7.1m from £4.2m the previous year and since then aggregate revenues have not fallen below £5.9m.

The club’s losses in FY19 were funded by a loan from Stefan Rupp of £1.8m on which no interest is payable. There was an additional bridging loan of £0.2m in June, 2020 which was repaid the month after (following receipt of McBurnie monies). With those funds the club now has cash in the bank to deal with contingencies and there is no plan for repayment of the outstanding director loan (of £1.8m).

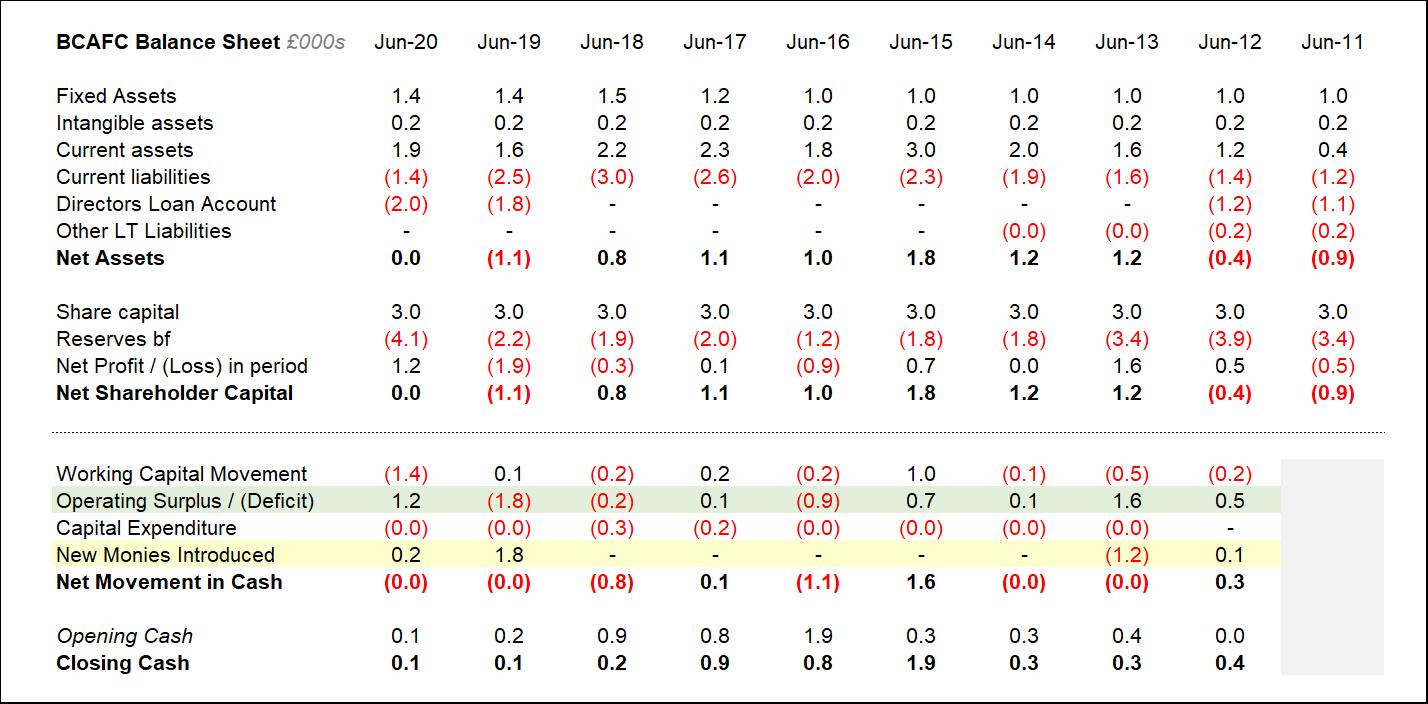

Since 2011 there has been a total of £0.67m capital expenditure invested in Valley Parade, of which £0.56m in FY17 and FY18. The fact that only £10k was expended in FY19 reflects the financial pressures of that season and a focus of investment on players.

In 2016, at the time of its sale, the club was free of debt. Now the only debt is the loan owed to Stefan Rupp although its substance is what could be described as quasi-equity. For instance, it is not the equivalent of a term loan borrowed from a bank, amortised (paid back) in monthly instalments. To that extent the club can say it has been free of external debt since the completion of payments under the former CVA.

The published financial statements are a lag indicator of performance. Furthermore, profit generation in a period is distinct from cash generation, demonstrated by the most recent FY20 accounts which show profit for the McBurnie sell-on clauses whereas the cash was not received until the current financial year (that is, after 30-Jun-20).

Whilst profit generation is obviously a key metric, the funding of a football club is equally a critical issue. What the annual accounts do not reveal is the pinch points that occur during the year when cash is tight, arising typically in the new year if there is no bonus of cup revenue or at the end of a month if cash flows are not sufficient to pay wages or the taxman.

The financial statements actually tell us very little about the cash pressures behind the scenes.

Click on the table to enlarge it

Click on the table to enlarge it

The future

No-one can spend money that they do not have or that they cannot afford – or want – to lose. Or rather, money that cannot be spent without implications if things go wrong. This was the dilemma facing Julian Rhodes and Mark Lawn who made no secret that they could not bankroll Bradford City in the Championship.

At the point that the club was on the brink of a possible return to the Championship they elected to sell to a party who could take City onto the next level. Hence, in 2016 the sale of the club to realise that ambition.

During the last ten years the club’s financial record should be compared with the likes of Sunderland, QPR and Coventry or clubs such as Colchester and Wigan who have been sustained through the charity of their owners.

There have also been high profile insolvencies where football directors have been unable to defy financial gravity indefinitely. Recently, Bury and Macclesfield have been victims of insolvency. Whilst other clubs have seemingly emerged unscathed from insolvency, an administration does not make liabilities disappear completely and it is a fallacy to believe otherwise that insolvency destroys value.

(There are plenty enough businesses in all sectors and industries who have emerged from insolvency but survive in a state befitting the description of being a zombie.)

Image by John Dewhirst (copyright Bradford City)

There are two ways in which Bradford City’s finances can be radically transformed to fund the ambition and risk-taking that has been called for on social media or the new stadium that has been suggested. Unearthing two or three McBurnies would go a long way to that end (or in the case of a new stadium, multiply that tenfold and more again).

The best guarantee however would be to persuade someone to throw money at the club. Nowadays, investing in a football club such as BCAFC would be contrary to most investment criteria and hardly the safest way to get a return on your money or safeguard a personal fortune. Who knows, maybe a billionaire with a passion for Bradford City could yet be found.

The opportunity however might equally appeal to those in possession of dirty money that could be laundered or to dubious investors from afar that no-one has ever heard of (as the example of Wigan Athletic attests).

Covid brings a whole new dimension to this and the prospect of an extremely difficult financial environment in the near term that makes owning a lower division football club an even less attractive proposition. I have not had sight of projections for the current season (FY21) although with the deteriorating Covid outlook it seems a reasonable bet that the club will be loss-making. Nevertheless, you cannot afford to lose sleep with nightmares. Instead, you have to look for the options upon which to build.

Although the Covid impact involves considerable uncertainty, there is genuine confidence that Bradford City is better placed to face the financial storms of the next few months than many other lower division rivals. For a start, even though the club voted against the salary cap regulations, it stands to benefit to a greater degree than smaller rivals.

An interesting development is the recent ‘Big Picture’ plan and the suggested redistribution of TV monies. The detail will be in the smallprint, but in conjunction with the salary cap it could potentially work to the club’s advantage by improving profitability.

According to press reports, League Two clubs would receive £2.5m annually, a not insignificant amount. Who knows, it could become the means by which BCAFC invests in infrastructure and training facilities or even buys back the Valley Parade freehold.

On the other hand, it would likely come at a big cost, for example an end to the traditional pyramid league structure and with other strings attached. Whilst the proposals are unpopular and have inevitable implications for the independence of the EFL, I expect that desperate clubs will snatch the bribe to ensure their survival. My feeling is that in the next few weeks this is going to be a real moral dilemma for supporters of all clubs outside the Premier League with implications also for the National League.

Photographer Alex Dodd/CameraSport

There is likewise the opportunity for Bradford City – and English/Welsh professional football – to reinvent itself. As I wrote previously on WOAP, the example of how Bradford Park Avenue adapted to wartime circumstances and focused on youth development is one such way.

Another lesson from history is the benefit of management stability and not changing the team manager every other year. From a medium-term perspective, the club is likely to derive further benefit from its youth academy and the potential for other talented young players to be sold. BCAFC will surely continue to derive advantage from its catchment in the Bradford Metropolitan District.

What the historic accounts demonstrate is that prior to 2016 the club had established a strategy of being self-sustaining and given the state of the balance sheet at the time of the insolvency, that was no mean achievement. In fact, it was probably contrary to all expectations.

Furthermore, the club’s relative profitability was better than in any other comparative period since Bradford City AFC had been formed in 1903. Julian Rhodes might be criticised for being invisible and adopting a low profile but still deserves credit for having kept the lights on at Valley Parade.

All of this was blown apart by the Rahic era. Nonetheless, the basis of a future self-sustaining model exists and places the club at a competitive advantage among its rivals (of which many are currently teetering on the edge of financial collapse).

Of course, it doesn’t constitute a sexy high stakes strategy. There is nothing glamorous about rigorous cost control and a focus on profitability but then, neither is financial failure and the personal tragedies that that entails. Nor is a focus on profitability common in English football despite most of us being familiar with the discipline in our day jobs.

The ability to control costs is not something that comes easy to every business and I suspect that a number of football clubs will find it difficult to implement economies. For those there will be a steep learning curve but irrespective, all will need to live within limited means in the brave new world.

With the next few months likely to bring multiple company failures, job losses and insolvencies there will be less sentimentality or spare cash to save insolvent football clubs. Besides, to enter a recession saddled with debt from a hostile, third party (external) lender is the stuff of nightmares – a prospect faced by a number of other football clubs although thankfully, not Bradford City.

The balance sheet of the club is what it is and history cannot be undone. The fact that Bradford City does not own Valley Parade remains a constraint and the legacy of under-investment is a handicap. Irrespective, ‘we are where we are’. Whilst it is easy to level criticism at BCAFC or highlight the weakness of its balance sheet, the club is actually in a far better position than many of its peers and as a consequence, more likely to survive. Nevertheless, there are no guarantees.

However, with the necessary focus and unity of purpose we might yet emerge stronger. The outlook will be difficult but if any comfort can be taken, the scale of the challenge is unlikely to exceed that which faced the club in 2004.

JD is a business turnaround specialist and was engaged by the club and the PFA in 2003 and 2004 to review its financial affairs. He has written books on the origins of organised sport in Bradford and the history of Bradford City and Bradford Park Avenue. His latest book, The Wool City Rivals: A History in Colour is published at the end of this month ( www.bantamspast.net ). He is currently working on another history of the two Bradford clubs and their financial affairs.

Categories: Opinion

Thanks for your support, have an amazing summer

Thanks for your support, have an amazing summer  Fascinating, isn’t it?

Fascinating, isn’t it?  What’s next for Bradford City?

What’s next for Bradford City?  The play-offs and Bradford City – a potted history

The play-offs and Bradford City – a potted history

Hello John

I note in your analysis and in your commentary that you have referred to the club’s turnover/tradng income. For example in 2019/20, you quote it as £6.7m. In the yearly analysis, you also provide details of the club’s operating costs. I don’t see any reference to the club’s turnover or its operating costs in the abridged accounts lodged at Companies House since the club chooses to only provide a balance sheet and not a P&L account. Have you been provided with additional information by the club on its turnover and operating costs for your analysis or do you have another source for the information other than the accounts presented to Companies House?

Thanks

The information has been accessed from the club’s (internal) management accounts.

Excellent write up John. Whitby Pete

Good info. Nice to see that level of transparency.

I know a lot of people constantly refer to the ground ownership / non ownership

Issue. But to buy it back seems inconceivable with these accounts. Not a viable return on investment. Such a long payback period so we are trapped in a cycle of renting. Laying out the cash to purchase would no doubt mean interest payments over a long term payback so would it be any better than renting? On the plus side the figures quoted above (300k in 2004 and 434k in 2019) means that rent increases are still below inflation over the same period. I think it would take a long term strategy (25+ years) to make any of this work and it would mean very controversial decisions. Like buying the ground back and then selling it To fund another development. But what’s the value of the ground and that land ? Who’s going to create a profitable development in that location with the associated demolition costs and ground clearance costs. As stated the topography is not forgiving there. What’s more It’s a tough economic climate especially in Bradford. Even stating requires significant and regular capital investment to maintain and keep up with an ageing asset.

I certainly don’t envy the owners and chairmen. Let’s hope Stuart can start making progress on the field and that can lay enough stability to make steady progress off it. CTID

You hit the nail on the head. These are the real life dilemmas that you don’t get on Football Manager computer games.

The stadium is ageing but at least the basic fabric is more robust than the original ground and unlike in the past there will not be the requirement to demolish stands or take a risk with spectator safety. The dominating theme in the origins and history of professional sport in Bradford has been urban geography which limits the options for where a sports stadium can be built (and probably also adds to the cost of what is achievable). The ability of the club to fund a new ground (or to expect Bfd Council to contribute) is pie in the sky which makes a complete mockery of those who have considered it feasible or petitioned the club to consider such a project.

The club has been criticised for not being ambitious but given its balance sheet constraints it is remarkable what was actually achieved prior to 2016. The more pertinent question is how the club can be ambitious in the first place.

Julian Rhodes has not done himself any favours by being invisible but I can understand why. Faced on the one hand with a balancing act to keep the club solvent and on the other to face the incessant criticism and guidance from those who demand ‘ambition’ is not a situation that I would envy and must be incredibly demoralising. It might also explain why he has retreated from public view.

Sorry, thick thumb syndrome strikes! Should have been an uptick!

Hi John,

Am I correct in assuming that any additional Ollie McBurnie monies received, in respect of Sheffield United retaining their Premier League status in 2019/20, will now fall into the FY21 accounts, due to late finish to the Premier League 2019/20 season?

Chris, fees re OMcB were recognised in FY20 but cash received after the year end.

Thank you an excellent summary.

Would be interested to know how you see the salary cap benefiting City over smaller rivals, I had thought it would suit the smaller clubs?

The smaller clubs benefit from a levelling-up that the salary cap brings which represents a competitiveness benefit, that is to compete with bigger clubs who could otherwise afford higher wages. For City, the benefit is principally one of profitability given that the salary cap brings a cost saving.

I am glad that the frequent (and daft) suggestion that SR is somehow taking money out of a business which barely turns a profit at the best of times can be put to bed. Interesting also to see the loan is interest free.

The fact that we have no “hard debt” and stable decent sized fan base gives us at least some hope for the future. There does need to be a conversation about season ticket pricing moving forward although I am sure this is an issue the club revisits internally frequently.

Those of a more speculative nature will no doubt deride the prudent approach taken pre Rahic. Personally the PP era built on sensible financial planning was something to buy into. What we paid through the gate (plus the odd player sale) determined what we put out on the pitch. To run the club in the black with such outstanding success on the pitch was considerable achievement. Sadly this is already forgotten by some.

What really is key though is that the clubs biggest asset is the loyalty and generosity of its support. We all know that this has been built up over generations in some families.Lets face it other than some great staff there is not a lot else in pot.

CTID

Barring the odd money laden loon who likes losing money, the lower leagues generate very little in terms of matchday income and TV broadcasting rights. A good discussion to be had is not just the future of Bradford City but also the future of lower league football, something which has been highlighted only recently by this ‘project big picture.’ A long term plan as to the landscape of football is paramount not just to the privileged few in the pemiership but also to the communities of smaller towns and cities whose club should be part of the fabric of the townsfolk. Football at the top level is no longer the game with the working class at its grass roots, now merely a vehicle for their owners to flaunt their wealth, i’m not sure i want to be a part of that.

Different gamblers adopt different strategies when they enter a casino. In this case the more fundamental question is about the football casino itself.

In my opinion Covid is bringing about the long overdue bursting of the football bubble and highlighting that the casino is no longer sustainable or maybe even desirable. In the next few months maybe we will see the big correction and I doubt that for some it will be pleasant.

I think Covid has made the decisions the EFL knew needed making but were too weak willed to do it, to the point clubs have gone to the wall despite supposed fit and proper test being done.

If you want to dine at the top table you need the bank balance to go with it. If you don’t it will eventually come crashing down as we found out only too well.

I agree, the EFL has been weak and its corporate governance has been ineffective.

What we are about to see in discussion of bailouts is failing / feckless clubs getting the bulk of the rescue. Ironically because BCAFC has benefited from the McBurnie monies and managed the balance sheet we will probably be considered ‘less-deserving’ than ‘Melchester Rovers’ which has run-up debts and losses in the pursuit of ambition. Therefore a big question of what moral hazard exists.

Difficult to avoid the conclusion that the way the game is run just stinks.

Yes, there’s something morally wrong with football that has got worse since the big TV deals have come into play. More money than ever coming into the game but who has actually benefitted?

Grass roots clubs still playing on mudbaths, parents and managers spending spare time fund raising for kit, while at the top, managers, players and worst of all, agents, milk the game for all its worth on the back of rising ticket prices and more TV subscriptions than you can shake a stick at. Have to agree with what you’ve alluded to, the game needs a reality check.

Agree with the sentiment mate. Sadly (and it goes against the grain for me)it will probably take Government involvement to resolve issues fairly and avoid another carve up by the big clubs. Like you having watched my kid over the years trying to play football on paddy fields and pitches rutted with car tyre tracks.A redistribution is long overdue

Thank you very much John for presenting a very informative article.

Many thanks for such a detailed and informative analysis.

Hi John,

Firstly just want to say a huge thank you for this article. Very much appreciated. A long read but a fantastic read none the less.

Two questions;

– You mention the salary cap for division 3 it’s currently £1,500,000 so this should mean we would make profit in the future as player wages will drop from previous years. Will this help us with capital going forward?

– Speaking of capital needed to buy back Valley Parade could it be possible for us to do what Chelsea did years ago under Ken Bates. Where people could buy upto 10 shares at a fixed cost ie £50. 10 shares x £50 per share = £500 x 10,000 season ticket holders = £5,000,000.

Thus creating a crowd trust owning the ground & getting rid of the annual rent we have to pay. Effectively Stamford bridge can’t be sold as it’s owned by the people. Would love to know if something similar could work in your opinion for Valley Parade.

Thanks again for the time dedicated towards this article. ⭐️

Certainly the only way it could get done. What was VP sold to Gibb for?

Thank you John for writing this thought provoking article.

Hindsight is a wonderful thing but what would supporters think about Geoffrey Richmond’s ‘six weeks of madness’ if the football club had have folded in 2004? The 1996 to 2000 period on the pitch was exciting but surely it wouldn’t have been worth it if had ended with no Bradford City to support? We have to adopt a conservative approach to spending money. What was achieved under Phil Parkinson still fills me with joy and pride. As for leaving Valley Parade, for me it’s a non-starter, owing to what happened on 11 May 1985.

As for the ‘The Big Picture’ plan, that’s another story. I’d like to know what David Conn thinks about it.

Couple of articles on already from DC. A cautious welcome at least as to the principle of a more equitable sharing of TV revenue. The chances of anything being agreed are slim with clubs self interest paramount are slim. It will probably take a few clubs going tits up to concentrate minds

The feature was written before the original Big Picture proposal was rejected. It will be interesting to see what comes of negotiations for revised proposals but we should be in no doubt that any gift from the Gods will come with costs and conditions that will compromise the independence of the EFL.

Excellent article.

Forgive my ignorance (or if i missed it) but am i correct to state that Rupp/Rahic therefore invested little when actually acquiring the club (not including the later 1.8m/0.2m loan)?

The director loan represents what has been injected in the club to keep it going. Whilst this was to fund trading losses, bear in mind it also effectively funded investment (capital expenditure) in the club / VP of £0.6m.

Thank you, its very good to see the facts presented to help minimise any unecessary speculation.

Much appreciated

Hi John

Excellent clear informed and balanced review.

I am very grateful not only for this work but also for all your efforts for the good of the club over many years now.

As you conclude not great – but apart from SR interest free loan no debt which is a real plus – as you know many SME’s and most football clubs are in a more precarious position – which is some comfort.

CTID

Paul

Clydesdale Bank hold a Debenture which is maxed-out at approximately £2 to 2.5 million. This Debenture has been renewed on an annual basis since about 2004. Notwithstanding Rupp the Club is indebted to the Clydesdale Bank and have been for many years.

Phil, Before you get excited with conspiracy theories of undisclosed debt, the charge is in place as security for Yorkshire Bank to cover potential exposure for the club’s BACs facility (for month end payroll) and credit cards. As it happens, Paul H (to whom you have replied) is an experienced banker and will be aware of such arrangements.

John, I am not implying any conspiracy theory or implying any wrong doing. I’m just stating for clarification that there exists a long standing Debenture which is a debt/liability. Surely this is undeniable and it represents a seven figure debt to City and Stefan Rupp. I’ve also stated this is a Line of Credit which is a common business practice.

I thought the purpose of this article was disclosure and “clearing the air.” Surely, with all the conjecture that currently exists your article is providing a valuable and much needed service. You should be commended for taking the time to research and write this article. My input on the Debenture was for clarification purposes only.

Phil I think you will find its a notional liability on the Stadium or the clubs “assets” generally to cover potential losses to the bank (if any) not debt in laymans terms. JD will correct me if I am wrong

Ps not the stadium for obvious reasons!

Paul in response to your message of 10:52am… yes you are correct about the debenture.

Notional liability is still debt and since City have no fixed assets required Rupps’ personal guarantee when he became owner.

Phil, please don’t get excited with conspiracy theories of undisclosed debt, the charge is in place as security for Yorkshire Bank to cover potential exposure for the club’s BACs facility (for month end payroll) and credit cards.

This really is an excellent piece which helps us all understand so much better the constraints City are operating under. While the Rahic ‘era’ was a disaster , I think we need to accept that Stefan Rupp is now acting with some integrity in making up for all those mistakes that his erstwhile partner inflicted on us. Without his current support we would be sunk.

The ownership issue of BCAFC needs to be resolved but it then begs the question who might be prepared to buy the club and whether they had the resources to invest after funding the purchase. The David Simpson regime is a good example of that – he acquired the club in 1990 and was hailed as a saviour by supporters but it soon became apparent that he didn’t have the money or the nous to revive it. My fear is that we might become prey to the unwelcome buyer, whether the Chinese gambler, Saudi prince or a criminal operation looking to launder money. For all his faults, Stefan Rupp has accepted a moral obligation to support the club and as an individual he is principled and decent which are qualities that cannot always be taken for granted.

Burnley have this very dilemma as they look for global investment. The club has been successful on the back of a very well run and organised off field. They should be careful what they wish for as what they have works.

Hi John, very much enjoyed reading your article. I do however have a couple of questions. The first is regarding your claim that in 2016 when Rupp purchased the Club that it was debt free. I seem to recall a Debenture held by Yorkshire Bank which was guaranteed and assumed by Stefan Rupp. I believe this £2 to 2.5 million Debenture is still outstanding and renewable on an annual basis which according to accounting practices is considered a Current Liability. This Debenture has been renewed on an annual basis for about the last 15 years and I would consider it to be debt owed by City/Stefan Rupp. Am I right or is this considered Rupp’s personal debt to the Bank and therefore not a City liability?

My second question is really to note something you appear to have inadvertently omitted or considered outside your time frame for review. That is the additional McBurnie windfall of £450k due for Sheffield United avoiding relegation last season. I expect it would show-up in this year’s financial figures since it falls due after the financial year cut-off of June 30th and therefore considered in this financial year 2020/21.

Phil,

(i) have a guess what that Clydesdale Bank charge might be in relation to;

(ii) the McB money you refer to was received in Aug-20 and will be recognised in FY21.

As I mentioned, i have not looked at the FY21 projections primarily because there is so much uncertainty. However, i also consider it inappropriate to be sharing detail of possible scenarios online – my duty of care and all that. My analysis has been based on a factual review of actual performance, not an assessment of forecasts.

Phil what do you think the additional Mcburnie money might cover? Its hardly burning a hole in Rupps pocket is it? How much more simply can the dire state of the clubs finances be put (not just now pretty much from the day we were incorporated) for the penny to drop. We are skint! Potless! Brassic! The only saving grace slightly less so than some of our competitors

Paul, I would suggest you take another look at the financial statement details and in particular the last four years. You will note the aggregate loss is £911k. A very modest loss for an EFL club. In fact, I think the financial results probably rank City in the top quartile for best performing clubs in the EFL. All thanks to the McBurnie windfall.

I honestly don’t consider that loss to be significant to a businessman reportedly worth £100 million. Heck, it’s less than 1%! We are not skint but we do have an owner who wishes he never heard of Bradford City.

It is a loss making business. A loss is a loss!!It always has been along with virtually all similar football clubs. Finding an EFl club that consistently turns a profit is like finding a needle in a haystack . Burton? Exeter? What personal wealth SR has is completely irrelevant. I am confused did you not read the article?

Phil, In response to your comment of 11:20am… It is very easy for us as supporters to advise Stefan Rupp what to do with his family inheritance and personal fortune. I would resent it and I suspect that you would too.

You are essentially asking for charity without necessarily offering anything else in return, other than to keep Bradfordians happy and give him a break from the abuse he suffers on social media. You are far better off providing SR with an economic incentive to invest instead of shamelessly begging.

John, I can definitely assure you that I’m not begging. How you came up with that thought is beyond me. I won’t expand any further on my opinion of Rupp but just to say the taxi’s waiting. End of discussion.

John, your right about the Debenture being currently held by Clydesdale Bank. I think the Debenture (Line of Credit) was maxed-out in September/October of 2018 and was one of the primary reasons for hiring Rhodes in a consultant role

I think you are jumping to conclusions. See response above.

Brilliant summary and analysis John.

Fully understood.

All I can add is its a good job that Nakki Delph Wisdom Cleverley Wyke and jackpot winner Mc Burnie came good.

Without that 9 million and nobody to undetwrite to that extent things would have been bleak.

As they are anyway.

Somehow Gibb should be pursuaded to sell.Alan ( B) once told me it probably stands him from the administrator at about 3 million.

A new ground would on basis of Rotherams cost be perhaps 30 to 40 million. To hold 20000 .

I see no more nuggets of gold.

Unless Staunton comes good.

How long will Rupp under write inevitable further millions in losses in this Brave new world?

He is not particularly interested in football.

All pretty depressing historic reading and the future looks tough.

John, many thanks for such a detailed and informative article coming from someone who knows what they’re talking about. this should put to rest some of the wild assertions, speculations and conspiracy theories eminating from some fans.

I am nowhere near a financial expert but might have a tiny bit more knowledge than the average man in the street. correct me if i’m wrong but this is how i read the current situation:-

By far the biggest drain on finances, the biggest drag on the club’s financial stability and progress is the annual rent on Valley Parade, currently running at £434K per annum and (on the present trajectory) set to be over half a million a year when the current lease expires in 2028. at that point the club will have to negotiate a new lease. it is a fact of financial life that, when leases are renewed rents go up, not down. the owners aren’t beneficiaries to the club. their aim is to maximise the income from their asset.

there is however a window of opportunity presented to the club by the salary cap. annual player salaries were £2.9million and they must reduce to £1.5million, presenting the club with an annual surplus of £1.4million.

I know that fans have talked about using that money for a top notch scouting system or a state of the art training ground but believe me, if you care about the wellbeing and future stability of Bradford City football club then a buy back of the ground must come first.

You quite rightly said that City were highly unlikely to find a bank or finance house prepared to provide a loan for any buy back. there is however another source. a source with intimate knowledge of the club’s finances and for whom any buy back of the ground would be hugely beneficial……I give you Stefan Rupp. he knows of the £1.4million that will become available because the club can no longer pay that out on player salaries. furthermore, if the club were to own Valley Parade once more then it would become financially sound profitable and secure. a much more inviting prospect for any potential buyer and at a much higher price than at the present.

this means nothing however without an answer to two questions……are the owners prepared to sell and would this be at a reasonable price acceptable to the club and it’s owner. if the club hasn’t already asked those questions of the Flamingoland pension fund then now would seem like a good time.

as an aside there is another aspect of the ground situation which is quite mystifying. Bradford council could have helped the club and perhaps put a little bit of pressure on the owners. to date they have conspicuously not done that. it is within the powers of the council to place a covenant on Valley Parade preventing the current or any future owners of the site from using it for anything other than a sports ground. it has already been done at grounds elsewhere in the country but, so far as i’m aware it has still not been done at Valley Parade.

Paul,

I would agree with your observations. I had not seen the detail of the accounts at BCAFC since 2004 and admit I was surprised by a number of themes, in no particular order:

(i) Whatever people might think of JR he has done a decent job of keeping the club afloat and operating with limited resources. I have been described as someone with rose-tinted glasses about BCAFC which amuses me greatly and to set the record straight, in 2004 I said to JR that it looked an impossible situation to revive BCAFC. At the time I was struck by his optimism and positivity. He is decried as being unambitious but I would counter quite the opposite. Besides he cannot be faulted for his deal doing with regards to McBurnie etc which has definitely saved the club. He is not a frontman but out of sight he has been pretty canny.

(ii) JR has demonstrated that a self-sustaining strategy is possible. You could argue that pre-2016 it was against the odds and at the expense of investment in infrastructure but nonetheless it kept the club afloat. Arguably the new salary cap (and more TV money?) makes it more likely that the club can be self-sustaining going forward.

(iii) The level of capex at the club has been minimal and ironically it has been the new owners who have invested in the ground. However it is clear that more expenditure is necessary.

(iv) From a glass half-empty perspective the balance sheet is dire. From a glass half-full it is not as bad as those of other clubs and actually quite respectable.

(v) The Covid situation is worrying in terms of implications but crucially there are potential opportunities to strengthen the position of the club. It is also a very fluid outlook and indeed during the course of the few days we have seen different options and proposals being suggested.

(vi) As you say, the whole VP / rental issue is a big issue and the rent / upkeep of the ground represents a major commitment and has been a major burden. We have paid out in excess of £3m in rent in the last ten years which is a massive amount.

The ownership situation has to be dealt with one way or another but I’d be surprised if a new buyer came forward in the next few months, let alone someone willing to pay a generous consideration. Anyone interested will play a waiting game to see how things work out. There is a strong argument as you have alluded, that if the club can be made self-sustaining and is not a drain on cash, Stefan Rupp would be no worse off retaining his investment and not crystallising a loss. In turn that makes a purchase of VP a quite different proposition.

Your point about the Council playing a role is also massively relevant. I have little confidence in the elected representatives at City Hall but they need to be reminded of the value of BCAFC to the city and how the club needs political support to ensure its future.

All told I believe that there is scope for an imaginative solution to this and with the right vision I am confident that a strategy can be formulated that all stakeholders – including supporters – can buy into. Post 1985 and 2004 it was demonstrated that with unity of purpose the club could overcome its difficulties and the same is required now.

BCAFC has the benefit that it does not have to make a decision in haste as a matter of distress and can afford to watch how the shifting sands move. Nevertheless it means that all scenarios need to be considered so that decisions can be made with the necessary understanding of what they entail. With imagination I do believe that a solution can be found to ensure the club’s survival.

When things eventually go back to pre covid times and now with a salary cap in place, would Bradford City’s average turnover in league 2 allow Stefan Rupp the ‘luxury’ of the club being slef sufficient, if you include the other costs such as ground rent and off field staff? If it does then Rupp is under no real pressure to sell.

As for Valley Parade, what is the best long term solution regarding ownership or renting? How does the rent cost relate to other league 2 clubs who are tenants and if Gibb was willing to sell would it be worth buying for long term?

Each of the scenarios need to be modelled and evaluated. The important thing is to approach with an open mind.

In terms of the Valley Parade the club have until 2028 until they have to negotiate a new one. It would be great if the fans can start this ball rolling and come up with a fighting fund to buy it VP back.

Can the fans raise the amount of cash needed? Whatcwould be the figure? Wimbledon fans have £30 million to rebuild and return to Plough Lane. Why cant we do something thing along similar lines?

Gven that the rent is roughly 440k a year Gibb’s pension fund is guaranteed roughly £4 million between now and 2028. It’s a win win for him. Would he really want to or need to sell? That seems to be a the sticking point.

The ground is not worth much in terms of real estate but worth a lot more to Gibb with current arrangement isn’t it?

It would take a big money offer for him to let the ground go. He cant lose as he doesn’t have the upkeep or maintenance of VP to worry about.

All the money raised is going into his staffs pension fund at Flamingo Land so I bet the money pays less tax and will be above the levels of other pension funds for staff working in a similar industry.

It would be real coup to own VP and gives us as a club something tanagabe to build on in the future.

The so called big six of the Premier Lg. are simply hell bent on total domination of all that goes on within the football pyramid. They might just as well send us all a sugar coated cyanide tablet. I would rather sell my so to the devil. !

Fascinating read. What we could really do with us a super rich double of Julian Rhodes!! Anyone know one?!

Thanks for the amount of time you have obviously spent in compiling your enlightening article John, much appreciated. There is often wild speculation as to the freehold value of VP, would you have any thoughts on a commercial value ? Another point of interest, with regards Mark Lawn’s £1m loan to the club, how much did it cost to repay it in 2013 ? Thanks again.

If you look at the abbreviated funds flow in the bottom table headed ‘Balance Sheet’, in FY13 you will see a negative figure of £1.2m in respect of funds introduced (line highlighted yellow). This represented funds repaid, being the settlement of the director loan which included interest. Equally you will see that the positive figure of £1.8m in FY19 represented funds introduced by way of SR’s director loan in that year.

As regards the freehold value of Valley Parade I would hate to guess. The valuation is difficult because it is a unique asset. By way of alternative use valuation it would be negligible not simply because it is Manningham but because there would be the cost of demolition of stands. Ultimately the valuation is determined by what someone is prepared and able to pay and what the other party is prepared to accept. My response is not intended to be facetious, rather to highlight the likely game of poker between the Gordon Gibb Pension Fund Trustees and BCAFC in the event that an approach was made by the club to buy the ground.

Than you for such a good read. It brings to mind an old saying “How do you make small fortune? Have a large one and then buy a football club” What I think this does show is how important it is to find good youth players and if we cant keep them how shrewd we have to be with clauses on transfers to ensure we scrape by. I’ll maybe think twice when calling other clubs feeder clubs

I was aware of some discussion between the club and Gordon Gibbs Pension Fund about 6 or 7 years ago. The club sent Jack Tordoff to represent the club in preliminary talks surrounding any potential sale of Valley Parade.

There are several points worth bearing in mind. From a legal point of view, the pension fund is administered by a group of trustees whose responsibility is to get the best return on their investment in the provision of funds/ Clearly taking the £400k plus rent from us is of greater benefit than selling the ground back to us at the moment.

A sum of over £5k was mentioned as a starting point towards further discussion. The land is worth £1m so clearly on that basis it would not be worth consideration. But it has a value as a stadium although difficult to quantify. It would cost £1m to demolish the stadium although some materials could be recycled and have a value.

I am only a simple fan and dont really understand these big figures

but

I do have some experience of being a buy to let landlord

so this is what I have worked out in my head

I would be really interested in whether it has any relevance or if I have understood what is written here

I cant cope with the big sums involved

so

I think to myself

I have a property which yields a guaranteed £5000 per annum with no costs to me

and someone wants to buy this and approaches me, even though I havent put them on the market

so

what would I sell for?

at best I might get a 5% return on the money

so I want £100,000

plus 20% more to tempt me to sell

so all told if the buyer offered me £125,000 I could see myself selling

however the rent on VP is £500,000

so it looks like an offer of £125000 x 100 …

or

£12.5 million would do it…

Does anyone, particularly John, who clearly does understand these things very well, have any comment on this calculation?

Would the Trustrees have a duty of care to their pensionholders to consider this seriously?

(I make no comment on where such a sum could be raised!)

Wollix

I think there is a good logic to what you say but equally, no property is worth more than what someone is willing and able to pay which definitely rules out the £12.5m valuation. The Trustees have an obligation to get the best possible return but that might be derived from simply rolling the lease forward. Given that the club is unlikely to be able to afford a new ground (a topic given prior coverage on WOAP and the general concession is that it can’t) then it could be that an extension of the lease becomes most likely.

There is a precedent with what happened at Park Avenue when the club finally secured the freehold from the trustees of Harry Briggs in 1947. What strengthened the case of the club was that the ground was in need of major repair that the landlord would be responsible for. The club was also able to play the card of seeking another ground. In the end the trustees sold the freehold to Bradford Park Avenue AFC. I am not sure that BCAFC have the same degree of bargaining power re VP given that the club has responsibility for repairs. It all makes for a pretty interesting game of poker when the lease expires, if not before.

So at the point of expiry, John, could City simply say ” thanks we will leave…” without penalty

( I am only asking legally, not emotionally/fans etc)

thanks

Wollix

I would assume responsibility for dilapidations which could be contentious but there’d be no point BCAFC threatening to leave if they didn’t have another venue to fall back on. Could be the wrong game of bluff!